.svg)

Good morning! We've reached the time of the year when it can be a challenge to scrape together a few headlines to write a newsletter. However, the ongoing war in Iran and the impacts on the entire energy complex make this year an outlier to that historic norm. I'll likely continue to lead with a good number of oil-related items because, as we all know, what happens with oil absolutely impacts our industry. We are living in times when these impacts will likely be more severe than anything seen since at least the 1970s, if ever.

WTI opened the week by surging roughly 3% back toward $105 per barrel on Monday, and if you woke up Monday morning thinking the weekend's diplomatic chatter might finally deliver some calm to this market… well, that didn't last long. Iranian missiles targeted the UAE, Tehran signaled tighter control over the Strait of Hormuz, energy infrastructure was hit, and a tanker was struck by drones near the strait — all before most of us had finished our first cup of coffee or Dr Pepper Zero. Brent briefly spiked to $114 per barrel, one of its highest levels since May 2022, before pulling back toward $110 after the U.S. denied Iranian media reports that an American naval vessel had been struck.

This is the pattern now: escalation, denial, partial retraction, price whipsaw. General Dan Caine, Chairman of the Joint Chiefs, told reporters Tuesday that Iran's attacks fall "below the threshold of restarting major combat operations," and Defense Secretary Pete Hegseth said the ceasefire "is not over." For some, those words are reassuring; for others, the bar seems a tad low. However, the market reaction seems to matter most right now.

To that end, WTI is trading near $103 as of this writing, having given back some of Monday's gains as the administration's posture steadied markets a bit, but the intraday range we're seeing is a sign that this market has its finger on a very live wire.

The underlying supply math hasn't improved. The IEA's April report estimated that global oil supply plummeted by over 10 million barrels per day in March — the largest disruption in history — with OPEC+ production alone falling 9.4 million barrels per day month-over-month. Goldman Sachs estimates total global oil stocks could fall to 98 days of demand by end of May, and while that's above emergency thresholds, the bank is flagging sharper localized shortages in South Africa, India, Thailand, and Taiwan — countries that can't just redirect to American barrels on a phone call.

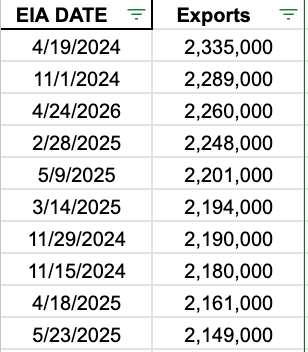

Here's the part of this story that matters most to our corner of the business. U.S. propane exports have jumped to roughly 2.260 million barrels per day and analysts expect exports to stay pinned at that level as long as the Strait of Hormuz remains closed. As we reported last week, the export total was the third-largest weekly total ever reported by the EIA:

As such, we are likely near the point of maximum export capacity, given current loading dock space, and the finite number of VLGCs that can export propane.

IF exports remain pegged to this higher level all summer long, it might help to keep a bit of a lid on propane inventories; however, we are already beginning this build season from record-high inventory levels, so propane prices will likely be driven by the War in Iran for the duration of our involvement. When a peaceful resolution is agreed upon and adhered to, propane values should struggle to find support. However, it's anyone's guess as to when that might happen.

In the meantime, American propane retailers are rapidly approaching the time of year when many will set prices for fall and winter programs. When you have very bearish fundamentals underpinning the industry, but flat price is reflective of a significant war premium, buying decisions are not easy. Cost-averaging and taking small bites to meet your needs seem like a sound strategy at the moment if you find yourself in this situation.